If you’re running a SaaS business in Japan, offering bank transfer payments (Furikomi) is critical for success. This payment method is deeply rooted in Japan’s business culture, especially for B2B transactions. While credit cards dominate in Western markets, Furikomi remains a trusted and widely used option in Japan.

Key takeaways from this article:

- Why Furikomi matters: Japan’s preference for Furikomi stems from its security, trust, and efficiency, particularly among older demographics and businesses.

- Regulations to follow: Compliance with Japan’s Civil Code, Payment Services Act, Electronic Bookkeeping Act, and APPI is mandatory. These laws cover transfer fees, digital recordkeeping, and data protection.

- Banking setup: Opening a Japanese business bank account involves detailed paperwork, identity verification, and compliance with anti-money laundering rules.

- Payment system integration: Automating bank transfer payments with virtual accounts and webhooks ensures accuracy and efficiency.

- Customer communication: Clear payment instructions, fee policies, and transaction limits are essential for smooth operations.

This guide covers everything from legal requirements to setting up your payment infrastructure, ensuring you can operate effectively in Japan’s unique business environment.

Step-by-Step Guide to Setting Up Bank Transfer Billing for SaaS in Japan

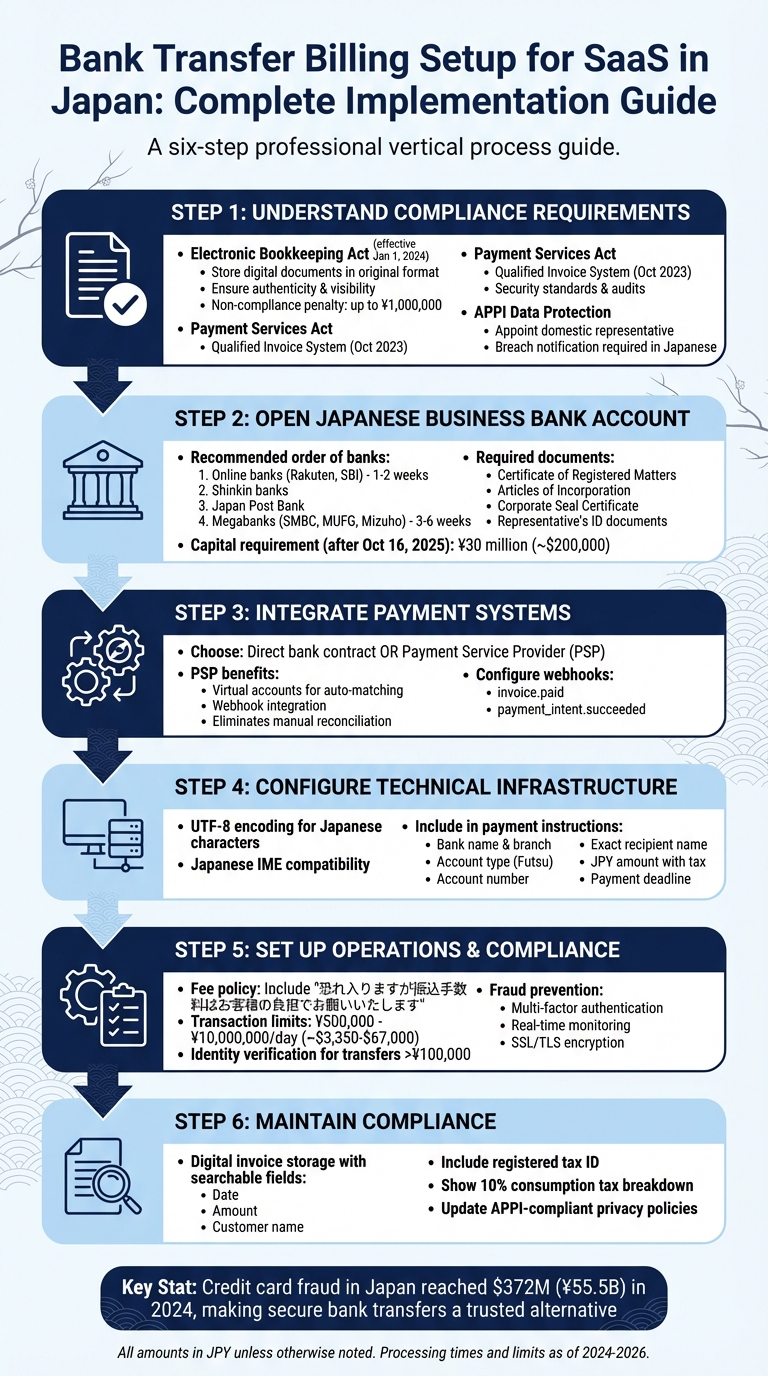

Key Regulatory Requirements

Operating bank transfer billing in Japan involves adhering to three major compliance frameworks. These frameworks set the rules for payment processing, record storage, and safeguarding customer data.

Electronic Bookkeeping Act Compliance

Starting January 1, 2024, the Electronic Bookkeeping Act requires all businesses, including SaaS providers, to store electronically exchanged documents in their original digital format. This applies to invoices, receipts, bank transfer statements, and files received via email, cloud platforms, or bank portals. Simply printing these documents and discarding the digital originals is not allowed.

The law emphasizes two key principles: authenticity and visibility. To ensure authenticity, businesses must prevent tampering by using timestamps, systems that log all edits and deletions, or formal administrative procedures. For visibility, storage systems must allow searches by transaction date, amount, and counterparty. Tax officials can request immediate access to these records, so having the right hardware at your storage location is critical.

Non-compliance risks include losing your "Blue Return" tax status, facing additional tax assessments, or incurring fines up to ¥1,000,000 under Company Law. Worse, if authorities find concealed or tampered data, an extra 10% penalty tax may be added to the standard 35%–40% penalty. On the upside, electronic receipts are exempt from Japan’s stamp duty, which applies to paper documents over ¥50,000 and ranges from ¥200 to ¥2,000.

Next, the Payment Services Act outlines further invoicing and security obligations.

Payment Services Act Requirements

In addition to digital recordkeeping, the Payment Services Act introduces specific formatting and security standards. While primarily aimed at electronic payment providers, these rules also affect bank transfer billing through requirements for secure systems and proper audits. For instance, invoicing systems must comply with the Qualified Invoice System introduced in October 2023. These invoices are necessary for customers to claim consumption tax credits and must be stored according to the Electronic Bookkeeping Act’s digital requirements to remain valid.

For fintech SaaS providers, the Financial Services Agency (FSA) enforces stricter measures, such as faster notification deadlines – sometimes within hours – and specific reporting formats. Even if your company isn’t classified as a payment service provider, implementing strong security controls and maintaining detailed audit trails can help meet overlapping regulatory expectations.

Alongside these payment-related rules, data protection under APPI adds another layer of accountability.

Data Protection Under APPI

The Act on the Protection of Personal Information (APPI) applies to any SaaS provider handling Japanese customer data, regardless of the company’s location. If your business operates outside Japan, you must appoint a domestic representative to work with the Personal Information Protection Commission (PPC) and handle customer data requests.

In the event of a financial data breach, you are required to notify both the PPC and affected individuals in Japanese, no matter how many are impacted. In typical SaaS setups, where the enterprise customer serves as the "business operator" (controller) and the provider acts as the "processor", it’s essential to notify customers immediately so they can meet their regulatory deadlines.

To streamline this process, you can prepare Japanese-language incident report templates in advance and define breach notification workflows clearly in your Master Service Agreements. These steps can help ensure a quick and compliant response during a data breach. Staying aligned with these regulatory frameworks not only supports seamless bank transfer billing operations but also safeguards your business and its customers.

sbb-itb-a752276

Setting Up Your Banking Infrastructure

After tackling compliance requirements, the next step is building a banking system that allows you to accept payments from Japanese customers. This involves opening a local business bank account, linking it to your billing software, and automating payment processes.

Opening a Japanese Business Bank Account

Opening a business bank account in Japan requires careful preparation and attention to detail. For foreign-owned SaaS companies, starting with online banks like Rakuten Bank or SBI Sumishin Net Bank is a good move since they often have higher approval rates. If your application is denied, try local Shinkin banks, then Japan Post Bank, and finally larger institutions like SMBC, MUFG, or Mizuho.

Applications must be done entirely in Japanese, and interviews are typically conducted in Japanese as well, highlighting the importance of localization for SaaS products in Japan. To apply, you’ll need to provide proof of a physical office, usually through a lease agreement. Banks may even conduct on-site visits to confirm your business location [15, 17]. Required documents include:

- Certificate of Registered Matters (履歴事項全部証明書)

- Articles of Incorporation

- Corporate Seal Certificate (印鑑証明書)

- Representative’s Residence Card, passport, and My Number Card for identity verification [15, 17]

Most banks still require a registered corporate seal (実印) and a separate seal for banking transactions. Processing times vary: online banks typically take 1–2 weeks, while megabanks may need 3–6 weeks.

If you’re applying for a Business Manager Visa after October 16, 2025, you’ll need ¥30 million (around $200,000) in capital and at least one employee. Be aware that banks are tightening their Anti-Money Laundering (AML) and Know Your Customer (KYC) policies through 2025 and 2026. This means they’ll dig deeper into beneficial ownership and transaction purposes [15, 16]. To improve your chances of approval, ensure your SaaS company has a professional website, a landline phone number, and a detailed business plan. Hiring an administrative scrivener (gyoseishoshi) can help you prepare documents in the correct Japanese format and avoid common errors that lead to rejection.

Once your account is set up, the next step is integrating it with your billing system for smooth operations.

Integrating Payment Systems

To handle growing transaction volumes efficiently, an automated payment system is essential. You can either work directly with a bank or partner with a Payment Service Provider (PSP). While direct bank contracts require manual reconciliation (which can quickly become overwhelming), PSPs streamline the process using virtual accounts [3, 18].

Virtual accounts are particularly helpful for Japanese bank transfer billing. In Japan, the recipient’s name must match the bank’s records exactly, and transfer fees can sometimes cause reconciliation errors [1, 3]. PSPs solve this by creating a unique virtual account number for each customer or transaction. This ensures payments are automatically matched to the correct invoice, eliminating manual errors [3, 18].

For subscription-based SaaS models, set subscriptions to "send_invoice" mode. If a customer’s virtual cash balance is insufficient for a recurring charge, the system will generate new payment instructions automatically. Additionally, use webhooks (like invoice.paid or payment_intent.succeeded) to trigger service activation as soon as the bank transfer is confirmed [18, 21].

Sending Payment Instructions to Customers

Once your banking system is integrated, clear and concise payment instructions are crucial to avoid delays or errors. Automated notifications should include all the necessary details:

- Bank name and branch name

- Account type (usually "Futsu" for ordinary accounts)

- Account number

- Exact recipient name as registered with the bank [20, 21]

Instead of relying solely on email, offer customers a hosted instructions page. This dynamic webpage can display real-time transfer statuses and step-by-step guidance. Adding your company logo and brand colors can increase trust and reduce concerns about phishing scams. Always specify the exact JPY amount (including tax) and set a clear payment deadline to keep records clean.

For domestic transfers over ¥100,000 (roughly $670), customers must complete identity verification at bank counters or ATMs [22, 23]. Be transparent about who covers transaction fees – whether it’s the sender or recipient. If you’re not using virtual accounts, encourage customers to include a reference note (like an order number) to assist with manual reconciliation.

Managing Operations and Finances

Once you’ve set up your banking system, the next step is managing daily operations. This involves keeping an eye on fees, adhering to transaction limits, and ensuring fraud prevention measures are in place.

Transaction Fees and Customer Communication

Under Japan’s Civil Code (Articles 484 and 485), customers are generally responsible for covering transfer fees unless stated otherwise . Many SaaS companies follow the "Our Burden (当方負担 – Toho Futan)" model, meaning customers handle the fees, ensuring you receive the full invoice amount. A standard note to include on invoices reads:

"恐れ入りますが振込手数料はお客様の負担でお願いいたします"

(Please note that transfer fees are the responsibility of the customer).

It’s important to set this expectation upfront in contracts. For existing customers, communicate any changes to fee policies clearly and directly. Keep in mind that fees can vary depending on the bank and transfer method, with some banks offering reduced or waived fees for transfers within the same bank .

Daily Transaction Limits

Japanese business bank accounts typically enforce daily transaction limits ranging from ¥500,000 to ¥10,000,000 (about $3,350 to $67,000). These limits are part of compliance with the Act on Prevention of Transfer of Criminal Proceeds and the Payment Services Act, designed to combat money laundering.

For SaaS companies handling high-value transactions, you can request higher limits through your bank’s online portal. Completing electronic identity verification (eKYC) early is essential, as unverified accounts may face strict limits as low as ¥300,000 per month . For example, in March 2026, Wise Japan allowed users with a registered Japanese address to send up to ¥150,000,000 (approximately $1 million) under its Type 1 license, while maintaining a ¥1,000,000 limit for adding or withdrawing funds.

Adhering to these limits ensures smoother operations while maintaining compliance with security regulations.

Fraud Prevention and Security

Fraud prevention is a must when handling integrated payment systems. In 2024, credit card fraud losses in Japan were estimated at $372 million (¥55.5 billion), with identity theft accounting for 93% of fraudulent card use in 2023. While bank transfers tend to be more secure than card payments, strong safeguards are still necessary.

To protect transactions, use multi-factor authentication (MFA) with SMS passcodes, hardware tokens, or biometric verification for all approvals . Setting custom transaction limits within your SaaS platform can also help reduce the risk of significant losses from unauthorized access. Implement real-time monitoring and configure alerts for unusual activity, transaction errors, or underpayments via email or SMS .

Additionally, encrypt all data transmissions with SSL or TLS protocols, restrict access to administrative tools from unknown IP addresses, and ensure your web applications and antivirus software are up to date. If you use virtual accounts through a payment service provider, these systems can quickly identify payment errors. Requiring the recipient’s name to match the bank account name exactly adds another layer of protection against manual entry mistakes.

Action Plan

To implement bank transfer billing effectively, follow these steps based on the outlined regulatory and operational guidelines.

Start by selecting your infrastructure approach – either open a Japanese business bank account yourself or collaborate with a Payment Service Provider (PSP). Direct contracts involve handling extensive paperwork and manually reconciling payments. PSPs simplify this process by automating payment matching.

Stay compliant with regulations: Maintain digital invoices with searchable fields like date, amount, and customer name. Include your registered tax ID and a detailed breakdown of the 10% consumption tax, as required by the Qualified Invoice System. Update your privacy policies to align with APPI standards. Proper electronic recordkeeping and data protection are critical for compliance.

Set up your technical infrastructure to support Japanese operations. Ensure your databases and APIs are configured for UTF-8 encoding to handle Japanese characters (Hiragana, Katakana, Kanji) and are compatible with Japanese Input Method Editors (IME). If you’re using a PSP, integrate webhooks to track payment events in real time, such as payment_intent.succeeded or payment_intent.partially_funded.

Clarify fee responsibilities in your contracts and invoices. Under Japan’s Civil Code (Articles 484 and 485), customers are generally responsible for transfer fees unless stated otherwise. To communicate this clearly, include the following phrase in your invoice remarks: "恐れ入りますが振込手数料はお客様の負担でお願いいたします" (Please note that transfer fees are the responsibility of the customer).

Once your system is in place, focus on managing transaction limits and ensuring proper data hosting. Prepare for operational challenges by requesting higher daily transaction limits (ranging from ¥500,000 to ¥10,000,000, approximately $3,350 to $67,000) through your bank’s online portal. Host data in regional centers to adhere to privacy standards.

FAQs

Do I need a Japanese entity to accept bank transfers?

You don’t need a Japanese entity to accept bank transfers in Japan. Services like Stripe make it possible through their Payment Intents API. Here’s how it works: Stripe creates a virtual bank account for your customer when they make their first bank transfer. This virtual account can then be reused for any future payments, simplifying the process.

That said, while a Japanese entity isn’t necessary for accepting payments, you might still need one for other business activities in Japan.

How do I automate matching bank transfers to invoices?

Stripe offers a way to streamline the process of matching bank transfers to invoices with its automatic reconciliation feature. Here’s how it works: Stripe assigns virtual bank account numbers to your customers, allowing them to make direct payments. Once the payment is received, Stripe automatically matches it to the correct invoice and marks it as paid. This system not only cuts down on manual work but also ensures accurate payment matching and handles retries for transfer payments, such as bank transfers, efficiently.

What do I need to store to comply with the 2024 digital record rules?

To align with Japan’s 2024 digital record regulations, it’s crucial to store electronic transaction records – like invoices and receipts – in a way that safeguards their integrity and prevents tampering. These records must be easily accessible for audits and meet the legal standards for electronic storage, ensuring they remain reliable and well-preserved over time.

Related Blog Posts

- Regulatory Compliance for SaaS in Japan: Key Rules

- Checklist: Localizing SaaS Onboarding for Japan

- Merger Control in Japan: SaaS Guide

- Japan SaaS Compliance: Data Storage Rules